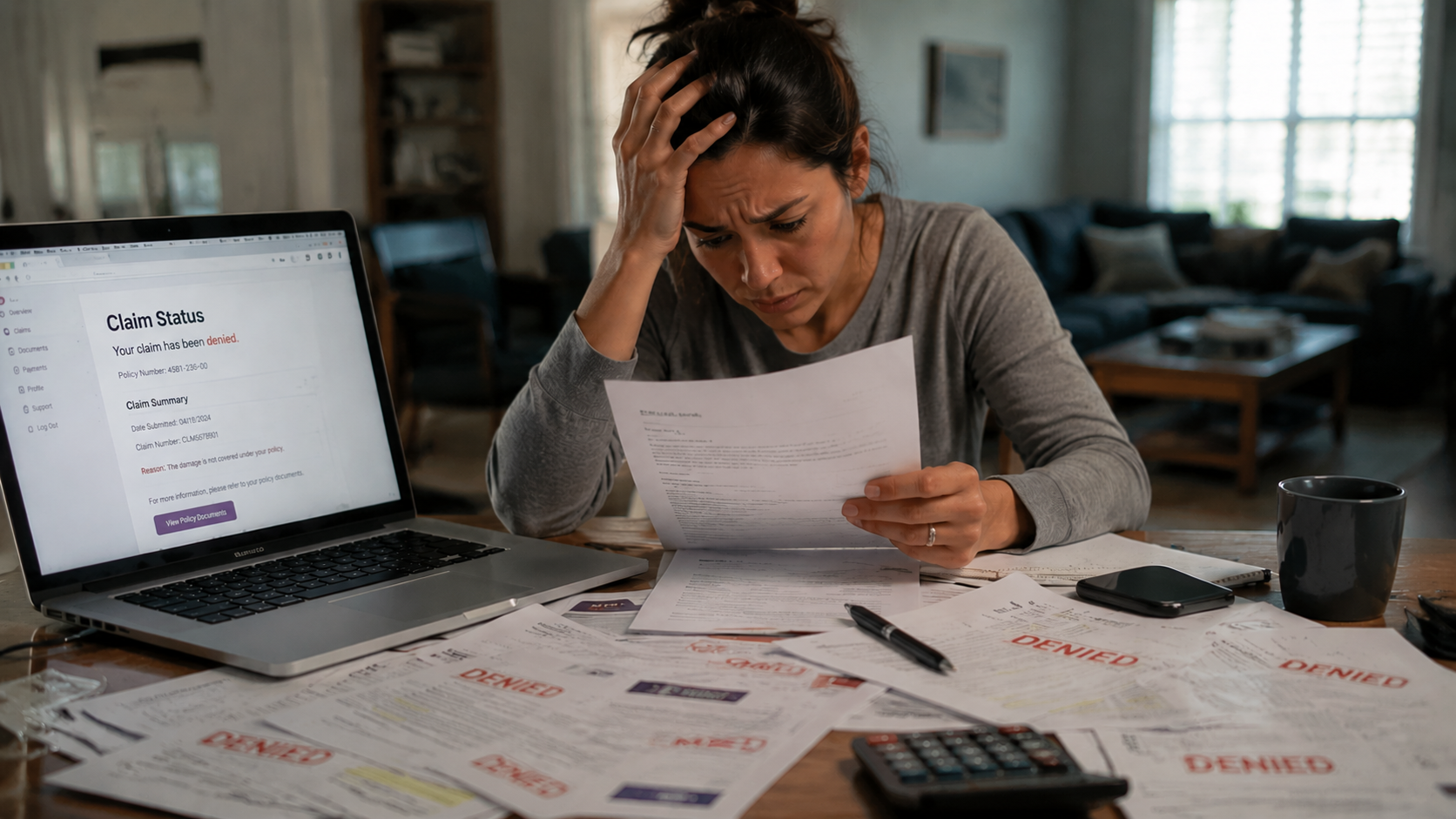

What to Do if Your Home Insurance Claim Is Denied

Why Was Your Home Insurance Claim Denied?

Understanding the reason behind the denial is the first step toward fixing it. Insurance companies must provide an explanation, but the wording can often feel vague or technical.

Common reasons claims get rejected

Some of the most frequent reasons include insufficient documentation, missed deadlines, or damage that falls under policy exclusions. For example, gradual wear and tear is often not covered under standard Home Insurance policies.

Policy exclusions you may have missed

Many homeowners are surprised to learn their policy excludes certain types of water damage, mold, or pre-existing issues. Carefully reviewing your policy details is critical before moving forward with an appeal.

Disputes over damage assessment

Sometimes the insurance adjuster and contractor disagree on the extent or cause of damage. This is where insurance claim help can be valuable in presenting stronger evidence and expert evaluations.

What Should You Do Immediately After a Denial?

Once you receive a denial, time matters. Acting quickly can help preserve your right to appeal and strengthen your case.

Review your denial letter carefully

The denial letter outlines the exact reason your Home Insurance claim was rejected. Highlight key phrases and compare them directly with your policy terms.

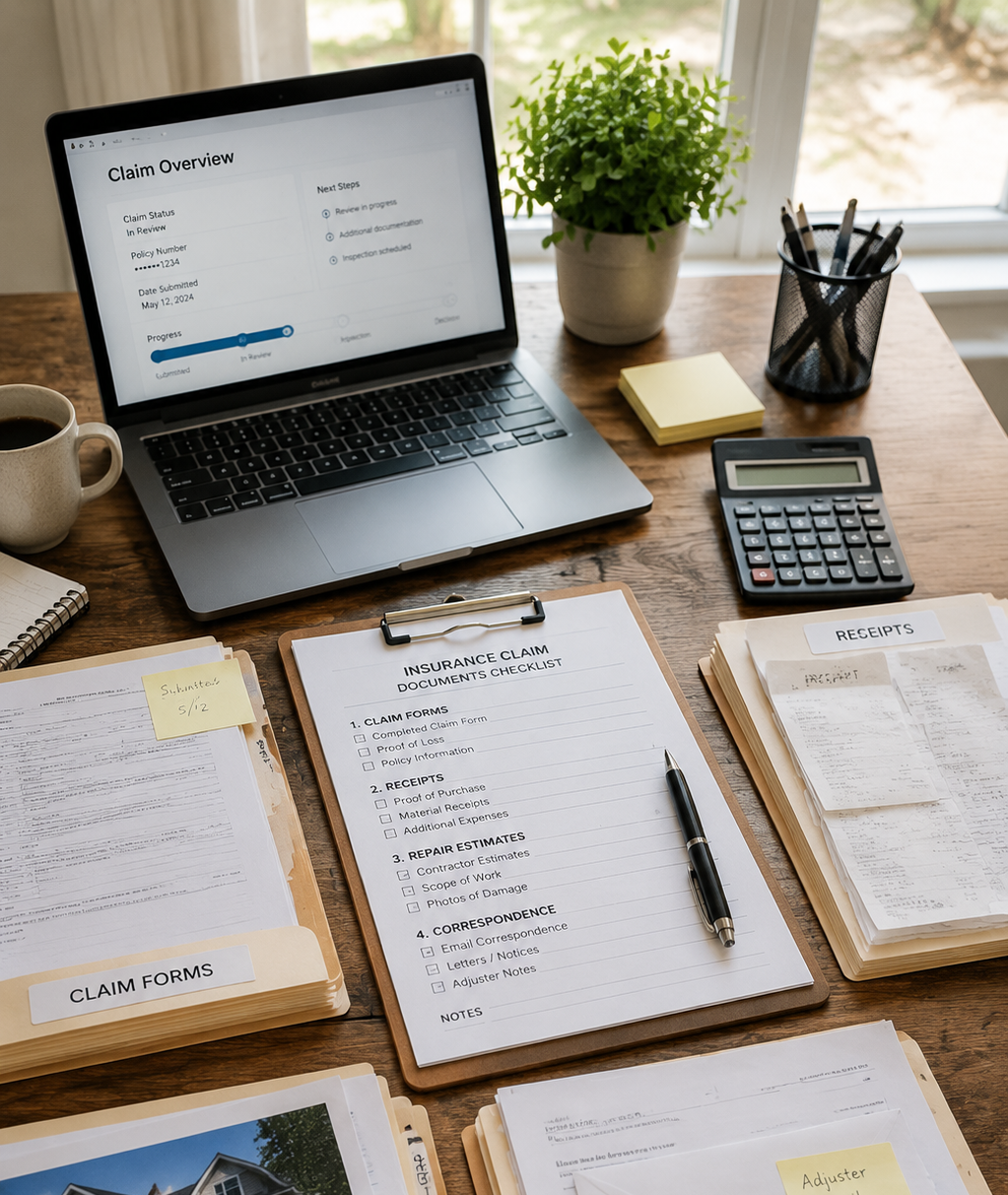

Gather supporting documentation

Collect photos, repair estimates, contractor reports, and any communication with your insurer. This documentation is often the foundation of a successful appeal.

Request clarification from your insurer

You have the right to ask questions. Sometimes a denial is based on missing or misunderstood information that can be corrected.

If you’re dealing with related coverage issues, you may also want to review your options for

Home Insurance in King George, VA to ensure your policy still matches your current needs.

How to Challenge a Denied Home Insurance Claim

Appealing a denial is not just about asking again—it requires strategy, documentation, and persistence.

File a formal appeal with new evidence

Most insurers allow you to submit additional proof. This can include contractor evaluations, engineering reports, or updated damage assessments.

Work with independent professionals

An independent adjuster can provide a second opinion that supports your claim. This is especially helpful in complex property damage cases.

Stay organized throughout the process

Keep a record of every phone call, email, and document submission. Organized files strengthen your position during review.

If your situation involves broader property coverage concerns, you may also explore

Business Insurance in King George, VA or

Auto Insurance in King George, VA to ensure all your policies are aligned.

When Should You Get Professional Help?

Not every denial requires outside help, but many homeowners reach a point where guidance becomes necessary. If your case involves large repair costs or repeated denials, getting insurance claim help can improve your chances of success.

Signs you need expert assistance

If your insurer continues to request the same documents or delays responses, it may be time to bring in experienced support. Complex denied claims often benefit from professional review.

Avoiding costly mistakes

Small errors in paperwork or missed deadlines can permanently affect your claim. Having someone review your case helps reduce avoidable setbacks.

Protecting your long-term coverage

Repeated disputes with your insurer can sometimes affect future coverage decisions. Getting the right guidance early can help protect your policy standing.

How Home Insurance Claims Impact Homeowners in Virginia

In Virginia communities like King George, storm damage, water intrusion, and unexpected repairs are common reasons for filing claims. When those claims are denied, it can leave homeowners facing financial strain and uncertainty.

Local homeowners often discover that policy details vary widely between providers. Understanding your coverage before damage happens is one of the most effective ways to reduce future denied claims and ensure better protection.

Call for Help With a Denied Home Insurance Claim

If your Home Insurance claim has been denied, you don’t have to deal with it alone. Olde Towne Insurance helps Virginia homeowners review denial letters, understand policy language, and take the next step with confidence.

Call Olde Towne Insurance today at

540-775-7070 for straightforward guidance and support on your denied claims and insurance concerns.

Frequently Asked Questions

Why would a Home Insurance claim be denied?

Claims are commonly denied due to policy exclusions, lack of documentation, missed deadlines, or disputes over the cause of damage. Reviewing your policy and denial letter is the first step to understanding the reason.

Can I appeal a denied insurance claim?

Yes, most insurance companies allow appeals. You typically need to provide additional documentation or evidence to support your case during the review process.

How long do I have to challenge a denied claim?

The timeframe varies by insurer and state, but many require appeals within a few months. It’s important to act quickly once you receive your denial letter.

Should I hire someone for insurance claim help?

If your claim is complex or involves significant damage, professional insurance claim help can improve your chances of a successful appeal. They can help organize evidence and strengthen your case.

A denied claim can feel like a setback, but it doesn’t have to be final. With the right steps, documentation, and support, many homeowners are able to overturn decisions and secure the coverage they expected. If you’re facing denied claims or need help understanding your options, contact Olde Towne Insurance at

540-775-7070 to move forward with confidence.

*This content is developed from sources believed to be providing accurate information. The information provided is not written or intended as tax or legal advice and may not be relied on for purposes of avoiding any Federal tax penalties. Individuals are encouraged to seek advice from their own tax or legal counsel. Individuals involved in the estate planning process should work with an estate planning team, including their own personal legal or tax counsel. Neither the information presented nor any opinion expressed constitutes a representation by us of a specific investment or the purchase or sale of any securities. Asset allocation and diversification do not ensure a profit or protect against loss in declining markets. This material was developed and produced by Advisor Websites to provide information on a topic that may be of interest. Copyright 2021 Advisor Websites.